solely .48 shipped!")

")

Picture supply: Getty Photos

These FTSE 100 and FTSE 250 shares look dust low cost proper now. Are they sensible bargains, or traditional investor traps?

Travis Perkins

Builders’ service provider and home-improvement retailer Travis Perkins (LSE:TPK) is again within the information on Wednesday. Sadly, it’s for the entire flawed causes.

Gross sales are crashing on the firm because the housing market cools and restore, upkeep and enchancment (RMI) spending sinks. Right now, it mentioned that like-for-like gross sales dropped 1.8% between July and September, a outcome that pressured it to scale back its full-year income forecast.

Adjusted working revenue is now tipped to vary from £175m-£195m, down considerably from an estimated £240m it spoke of simply two months in the past.

Travis Perkins shares have fallen round 7% on the information and are buying and selling round 52-week lows. So the enterprise now trades on a ahead price-to-earnings (P/E) ratio of 10.8 occasions. This sits simply above the extensively regarded worth benchmark of 10 occasions.

However I imagine the corporate deserves such a low ranking. The UK financial system is tipped for a protracted downturn, whereas higher-than-usual rates of interest additionally look set to persist. Subsequently, any turnaround in its finish markets could possibly be a great distance off.

Travis Perkins has an enormous retail footprint, which ought to put it in a great place when situations finally enhance. However the prospect of sustained income strain and a steadily-rising debt pile nonetheless makes it one low cost share I’m eager to keep away from. I imagine it’s share worth might preserve collapsing.

JD Sports activities Trend

Sportswear/life-style retailer JD Sports activities Trend’s (LSE:JD.) shares have been on my watchlist for a while. And following heavy share worth weak spot in 2023, I’m fascinated by making it my subsequent share purchase. Right now, the FTSE 100 firm trades on a ahead P/E ratio of 10.6 occasions.

On the one hand, the low valuation of JD shares could possibly be thought of honest given the unsure outlook for the world financial system and due to this fact shopper spending. Sellers of premium merchandise like branded sportswear and trainers could possibly be thought of particularly weak to buyer cutbacks.

Nonetheless, the retailer’s resilience despite current difficulties suggests this rock-bottom ranking is undeserved. Natural gross sales soared 12% in the course of the six months to July, with revenues helped by market share positive aspects in key markets.

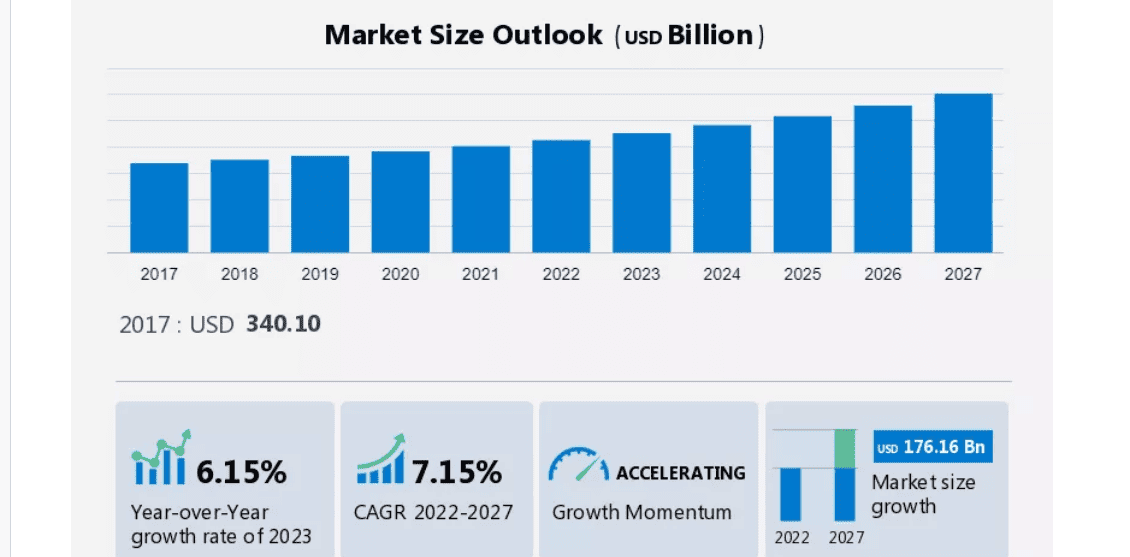

As a long-term investor there are two issues I’m particularly enthusiastic about on the subject of JD shares. Firstly, the worldwide athleisure (informal sportswear) market is tipped to proceed rising strongly, because the graphic beneath reveals.

Secondly, the corporate stays dedicated to fast enlargement to completely capitalise on this chance. JD — which operates greater than 3,300 shops throughout Europe, North America and Asia — is on target to open 200 new shops within the present monetary 12 months alone. It’s additionally investing closely in its e-commerce channels.

Analysts at Shore Capital lately described the corporate as “materially undervalued”. I’ll be trying so as to add JD shares to my portfolio once I subsequent have money to take a position.

The contents throughout the article have been equipped by way of Newswire for Finencial.com, go to

{kind=link}