solely .48 shipped!")

")

This previous week has been a doozy. We’ve received the same old headwinds piling up, with sticky inflation, a 1-in-3 probability for an additional Fed rate of interest hike this yr, and rising bond charges placing strain on shares. And if that wasn’t sufficient, the geopolitical scenario has heated up, with a serious warfare within the Center East as Israel goes to warfare in retaliation for Hamas’ newest atrocities.

However there are alternatives available in the market, and buyers mustn’t lose hope, regardless of the headwinds. The strategists at funding powerhouse BlackRock put it in clear phrases: “A difficult macro backdrop doesn’t imply a dearth of funding alternatives. Fairly the other, in our view. Larger macro volatility is translating into higher divergences in safety efficiency relative to broader markets. That requires a lot higher selectivity and extra granular views. Harnessing the mega forces shaping our world can even supply ample funding alternatives. All of it boils all the way down to what’s priced in.”

Turning these phrases into motion, BlackRock, the world’s largest asset supervisor with $9.42 trillion in property beneath administration as of the tip of Q2, has been actively searching for out these alternatives. It has just lately made important purchases of two high-yield dividend shares, with one boasting a yield as excessive as 9%.

We ran these tickers by TipRanks’ database to find out whether or not the Road’s analyst corps agrees that these are ripe for the choosing at current. Let’s take a more in-depth look.

Hannon Armstrong (HASI)

We’ll begin with Hannon Armstrong, an organization that’s been placing its cash the place its mouth is in the case of local weather change. This Annapolis-based agency leads the way in which in climate-positive investments and inexperienced initiatives, funding ventures in power effectivity, renewable power, and sustainable infrastructure. The corporate has a coherent imaginative and prescient for its investments, that all will enhance our collective local weather future.

Moving into some specifics, Hannon Armstrong’s funding portfolio at present totals some $4.9 billion. Of this, 51% is put into ‘behind-the-meter’ tasks, or power effectivity, distributed solar energy, and energy storage initiatives. One other 42% of the entire is in ‘grid related’ energy property, notably in wind and solar energy era and in energy storage. And at last, 7% of the portfolio is put into fuels, transport, and nature: that’s, renewable pure fuel, fleet decarbonization, and ecological restoration.

Whereas there was some controversy over the standard of ‘inexperienced’ financial and infrastructure initiatives, Hannon Armstrong has made cautious picks in its portfolio investments to return constant quarterly earnings. A part of the corporate’s aim is to indicate that climate-friendly investments can present sound returns for buyers. Within the final reported quarter, 2Q23, the corporate continued on this path, with a prime line of $74.33 million. This was up greater than 18% year-over-year, and beat the forecast by over $43 million. The agency’s 53-cent non-GAAP distributable EPS determine was in-line with expectations.

This will get us into HASI’s dividend determine. The corporate’s most up-to-date dividend declaration, made on August 3 for an October 11 payout, was for 39.5 cents per frequent share. At this price, the dividend annualizes to $1.58 per share and has a strong ahead yield of 9.3%.

BlackRock is clearly impressed by Hannon Armstrong, and is displaying that in essentially the most direct method attainable. The agency has, for the reason that finish of Q2, bought nearly 9.05 million shares in HASI, and now has a complete holding within the firm of 17,750,428 shares. The stake represents an possession share of 16.5% in Hannon Armstrong, and is value $298.38 million at present share value.

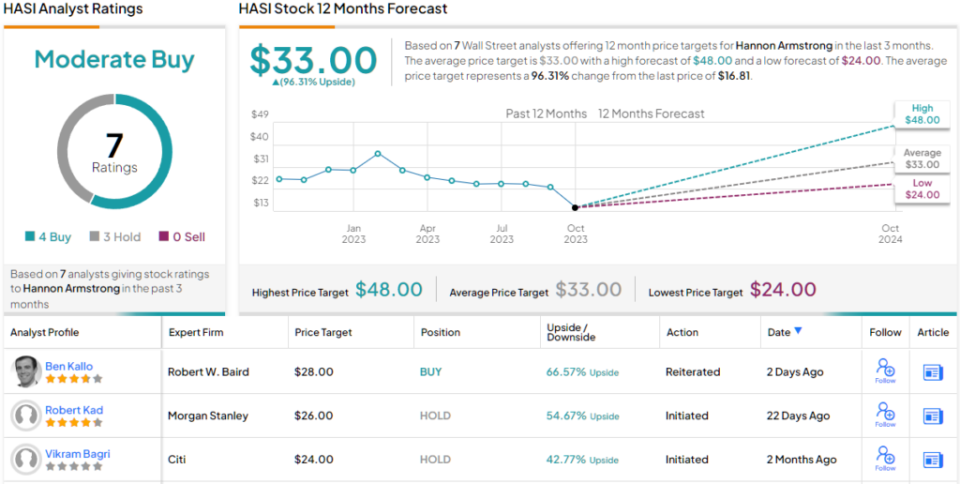

HASI shares have been unstable just lately, and they’re down some 31% for the reason that center of final month. Nonetheless, Baird analyst Ben Kallo thinks the dimensions of the drop is unjustified and factors out that the inventory has lots for buyers to love.

“HASI’s current selloff was partially in response to look NEP lowering its dividend development outlook and citing a more difficult surroundings amidst increased rates of interest. In our view, weak point in HASI shares attributable to NEP’s outlook doesn’t give credit score to HASI’s differentiated portfolio and powerful monetary place. HASI’s tasks additionally include working property vs friends which embody property in improvement in lots of circumstances, and we view this as a aggressive benefit,” Kallo opined.

“Larger rates of interest and worsening client well being have raised issues about near-term development alternatives. Regardless of the unsure outlook from others within the house, we consider HASI is about up for a powerful Q3 and see a clear quarter as a possible catalyst,” Kallo goes on so as to add.

In Kallo’s view, these information assist an Outperform (i.e. Purchase) ranking, and whereas his $28 value goal makes room for ~67% development over the following 12 months. Based mostly on the present dividend yield and the anticipated value appreciation, the inventory has ~76% potential whole return profile. (To observe Kallo’s observe report, click on right here)

Total, the 7 current analyst evaluations on Hannon Armstrong break all the way down to 4 Buys and three Holds, for a Average Purchase consensus ranking. The shares are buying and selling for $16.81, and their $33 common value goal suggests a one-year acquire of 96% for the inventory. (See HASI inventory forecast)

Gaming and Leisure Properties (GLPI)

Subsequent on our checklist is a REIT, an actual property funding belief, however one with a twist. Gaming and Leisure Properties, as its title suggests, focuses its investments on the acquisition, financing, and possession of actual property properties that are then leased out to gaming and on line casino operators. The corporate’s traditional lease is a triple-net lease association, making the tenant liable for facility upkeep, insurance coverage, utilities, and property taxes.

The enlargement of authorized on line casino gaming within the US in recent times has been helpful for Gaming and Leisure, and on the finish of 2Q23 the corporate had 59 gaming properties and associated amenities unfold throughout 18 states. These amenities whole greater than 30.2 million sq. toes of improved gaming house.

The corporate’s Q2 report additionally confirmed whole revenues of $356.59 million, up greater than 9% from the previous-year quarter. This whole, which beat expectations by nearly $1.3 million, included rental revenue of $319.24 million, for a ten% y/y improve. The corporate’s backside line determine, an EPS of 59 cents per share, was 7 cents higher than anticipated.

Of explicit curiosity to dividend buyers, GLPI additionally confirmed an adjusted funds from operations (AFFO) of 92 cents per share. This metric, which immediately helps the quarterly dividend fee, beat the forecast by a penny. The inventory dividend, of 73 cents per frequent share, was declared on August 30 and paid on September 29; the 73-cent fee represented a 1.4% improve from the earlier quarter. On the new price, the dividend annualizes to $2.92 per share, and yields 6.2%.

Turning to BlackRock’s stance on GLPI, we discover that the asset supervisor has acquired 12,230,081 shares of the REIT for the reason that finish of Q2. BlackRock now holds a complete of 30,622,204 shares within the firm, which have a complete worth of practically $1.43 billion – and which give BlackRock an 11.7% possession within the firm.

The inventory has gotten optimistic consideration from the Road’s analysts, too. Mitch Germain, writing from JMP, sees lots to understand right here, writing, “We’re constructive on the corporate’s embedded development pipeline, whereas including a brand new tenant to the portfolio solely enhances the potential for future funding alternatives. We proceed to view the corporate in a optimistic gentle, as rental revenue stream provides constant money stream with predictable development, administration’s popularity within the business is unparalleled, thereby offering it a glance into all offers within the house, whereas alignment is a optimistic. The diversification of GLPI’s funding technique to embody development funding has produced extra proprietary deal stream and helps ahead development prospects at elevated returns, in our view.”

“GLPI’s shares at present commerce half a flip under the net-lease REITs common at 12.4x, which we view as unwarranted, because it doesn’t appropriately credit score the corporate’s high-quality sturdy money flows, above-average development prospects, and traditionally low leverage,” Germain summed up.

These bullish feedback again up Germain’s Outperform (i.e. Purchase) ranking on the inventory, whereas his $57 value goal implies ~21% one-year upside potential. (To observe Germain’s observe report, click on right here)

All in all, GLPI will get a Average Purchase ranking from the Road’s consensus, based mostly on 13 current evaluations that embody 9 Buys to 4 Holds. The inventory’s common value goal of $54.21 suggests it should acquire ~15% from the present share value of $47.21 over the approaching yr. (See GLPI inventory forecast)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally necessary to do your personal evaluation earlier than making any funding.

The contents throughout the article have been provided by way of Newswire for Finencial.com, go to

{kind=link}