solely .48 shipped!")

")

Financial indicators are launched each week to supply perception into the general well being and efficiency of an financial system. They function important instruments for policymakers, advisors, buyers, and companies as a result of they permit them to make knowledgeable choices concerning enterprise methods and monetary markets. Within the week ending February 8, the SPDR S&P 500 ETF Belief (SPY) rose 1.86%. The Invesco S&P 500 Equal Weight ETF (RSP) was up 0.29%.

Whereas the financial calendar for final week featured a lighter load, three noteworthy financial experiences warrant consideration: the quarterly family debt and credit score report, the companies sector PMI, and the commerce stability. These knowledge factors can collectively present insights into varied elements of the financial system, together with client habits and repair sector well being. On this article, we are going to summarize the most recent knowledge on every of those indicators.

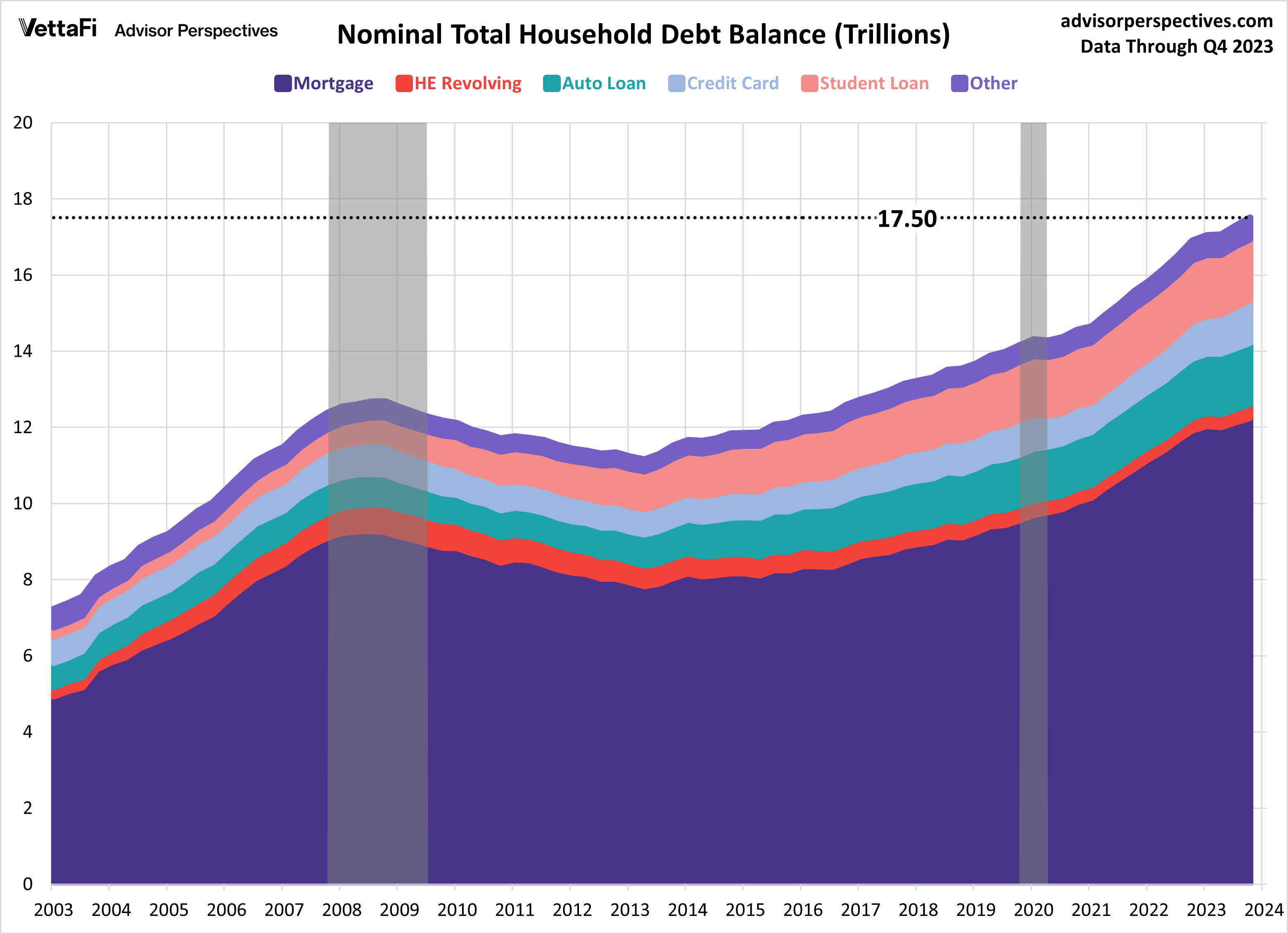

Family Debt and Credit score

Within the newest quarterly family debt and credit score report launched by the NY Fed, we noticed a notable $212 billion uptick in family debt, reaching a report $17.50 trillion in This fall. The most recent knowledge represents a 1.23% improve from Q3’s debt stage of $17.29 trillion. For a second straight quarter, all debt classes grew; nevertheless, the most recent surge was primarily fueled by elevated mortgage, bank card, and auto mortgage balances. Particularly, mortgage balances hit an all-time excessive of $12.25 trillion (a 0.9% improve), bank card balances reached a report excessive of $1.13 trillion (a 4.6% improve), and auto mortgage balances climbed to a report excessive of $1.61 trillion (a 0.8% improve). This complete report serves as a gauge for the monetary situations of U.S. households, providing insights into their financial well-being.

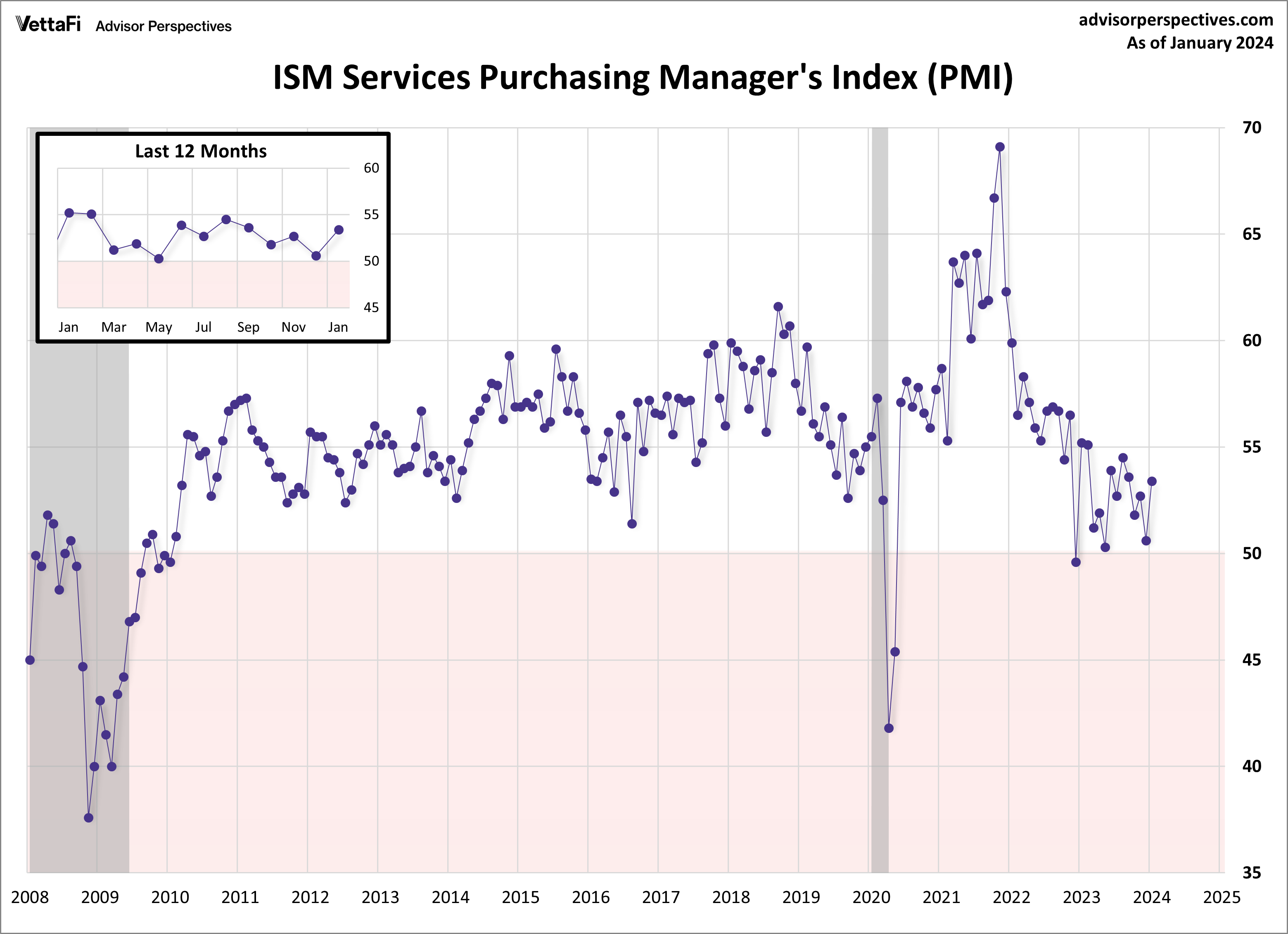

Providers PMI

Financial exercise expanded within the companies sector for a Thirteenth-straight month. The ISM Providers PMI reached its highest stage prior to now 4 months, coming in at 53.4 in January. The most recent studying was higher than the anticipated 52.0 forecast. Practically all subcomponents of the index improved in January, with inventories being the only element that contracted. Moreover, 10 service industries reported development, whereas seven industries reported a decline. General, the enterprise situations within the companies sector are at the moment steady, because the sector has now grown in 43 of the previous 44 months; the lone contraction was in December 2022. Notably, many respondents reported optimism concerning the financial system on account of potential rate of interest cuts, however in addition they stay cautious about inflation, value pressures, and ongoing geopolitical conflicts.

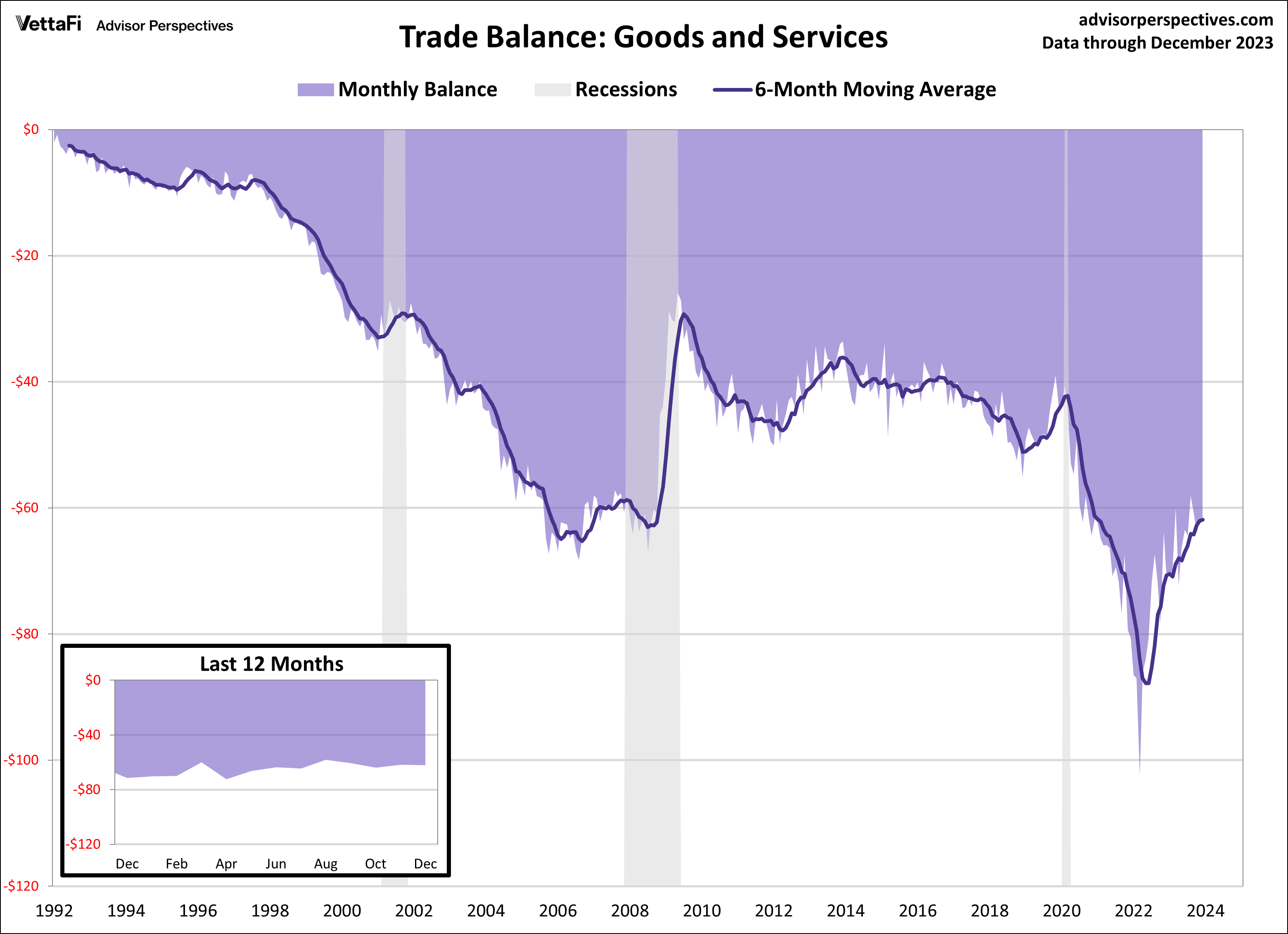

Commerce Stability

The U.S. worldwide commerce deficit expanded greater than anticipated in December on account of a bigger improve in imports than exports. The commerce deficit elevated by 0.5% in December to $62.20 billion, bigger than the $62.00 billion forecast. Exports rose by $3.9 billion (1.5%) to $258.25 billion whereas imports rose $4.2 billion (1.3%) to $320.45 billion. The commerce stability, which experiences on the nation’s imports and exports of products and companies, supplies insights into overseas commerce dynamics, serving as a gauge for the general development or contraction of the financial system. The deficit has now grown in three of the previous 4 months. Nevertheless, regardless of the current development, the deficit has shrunk 11.4% in comparison with the beginning of the 12 months, and is 12.9% smaller in comparison with a 12 months in the past.

Financial Indicators and the Week Forward

The upcoming week will function the most recent inflation, client spending, and client sentiment knowledge. On Tuesday, the Bureau of Labor Statistics will launch January’s Client Worth Index (CPI). Then on Thursday, the Census Bureau will launch retail gross sales knowledge for January. Lastly, on Friday, the College of Michigan will launch its preliminary report for its Client Sentiment Survey for February.

Present forecasts present that headline and core CPI elevated 0.2% and 0.3% from December, respectively. Retail gross sales, which is able to impression pursuits within the SPDR S&P Retail ETF (XRT), are anticipated to extend for a third-straight month, rising 0.1% from December. Lastly, the preliminary report for the Michigan Client Sentiment Index, which may impression curiosity within the Client Discretionary Choose Sector SPDR ETF (XLY), is predicted to extend from January’s remaining studying of 79.0 to 80.0.

For extra information, info, and technique, go to the Modern ETFs Channel.

The contents inside the article have been provided through Newswire for Finencial.com, go to

{kind=link}