solely .48 shipped!")

")

Nearly each monetary establishment invests a variety of effort and cash into enhancing buyer expertise (CX) within the banking service they supply. That is the primary manner to make sure a aggressive benefit within the digital age. Sadly, generally

outcomes are pitiful. What may very well be the explanations behind a foul end result of digital product design in monetary business?

1. Digital Buyer Expertise of a Monetary Product shouldn’t be Related to its Model

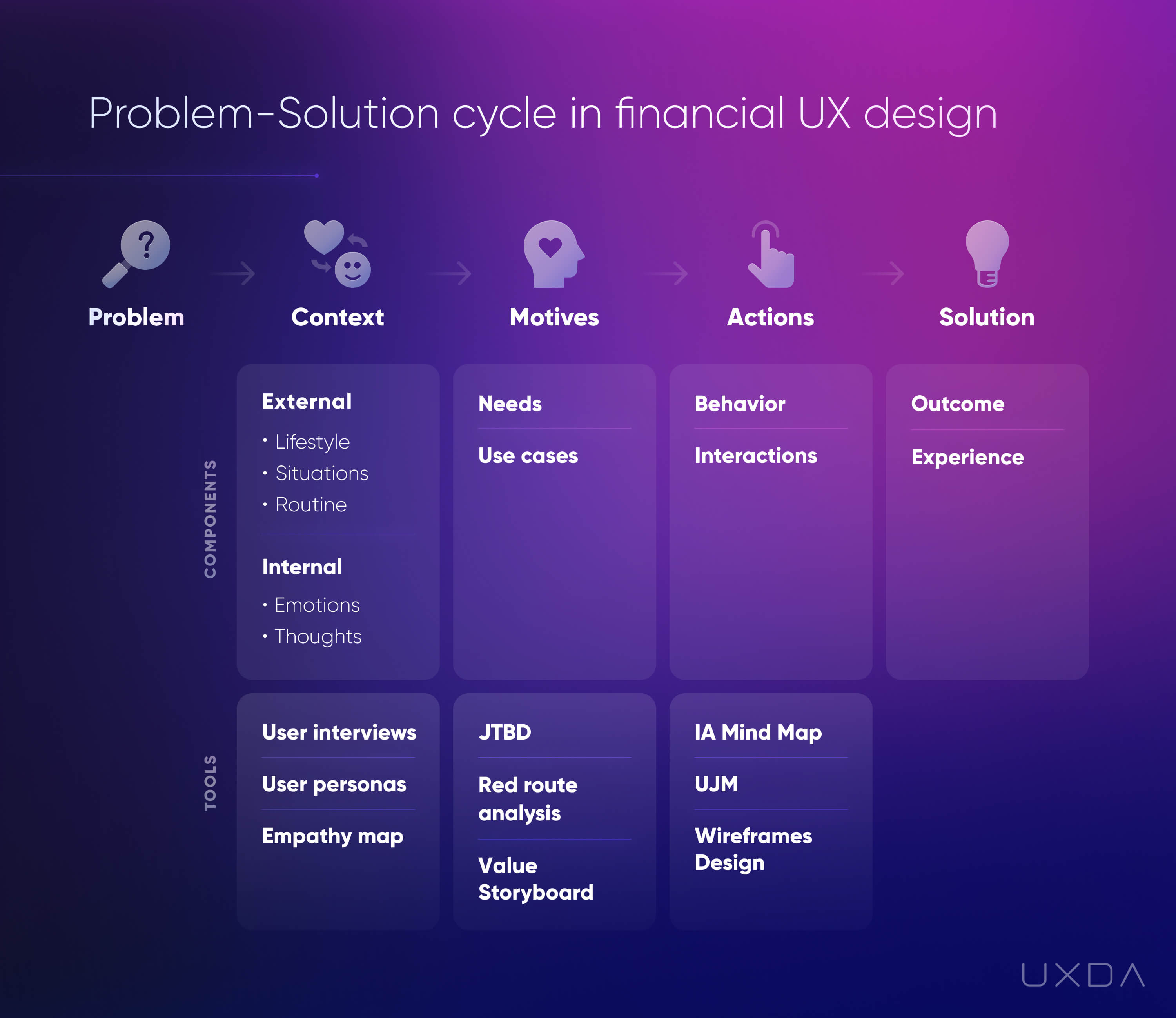

It is not sufficient to copy the design of one other properly wanting monetary app to make sure a terrific high quality digital buyer expertise in monetary product. Behind each digital transformation success, there’s various distinctive components that impression the banking

buyer expertise. Person interface design is just a kind of.

For a digital product to succeed it is essential to bear in mind your model uniqueness, buyer expectations and cutting-edge expertise. To show your digital service right into a long-term aggressive benefit, conduct person analysis and execute a tailored

monetary CX engineering.

2. The Curse of Information

When somebody is speaking with others, unconsciously believing that they might have the very same context to completely perceive what he is saying, it is referred to as a cognitive bias.

In lots of instances, the identical occurs when finance professionals create a digital service that they consider is straightforward and nice to make use of, whereas clients are confused by its complexity.

To architect the absolute best buyer expertise in monetary providers, converse the “clients’ language”, develop into their ally. You possibly can obtain it by means of in-depth empathy, data of psychology, monetary CX analysis, usability testing and user-centered

enterprise mindset.

3. False Hopes

There is no doubt in regards to the impression of design in creating profitable digital merchandise. Nevertheless, it is defective to imagine that excellent design in monetary providers is the one factor FIs want to achieve prompt success.

Even digital merchandise with nice monetary person expertise (UX) are nonetheless topic to market guidelines and a number of enterprise components, just like the enterprise mannequin, technique, the way in which product’s launched available in the market, the CX of assist, the rivals’ gives, and so on.

Managing all of those elements with the fitting allocation of accountability permits to develop into extra sure that the brand new digital product would actually succeed.

4. Lack of Monetary CX Experience

Very often FI executives outsource monetary service buyer expertise designers hoping that in a number of months they’re going to convey a brand new profitable app design to the desk. Sadly, this type of situation very not often works out. The success of a monetary

app relies upon not solely on the design expertise of the designers however most significantly on an in-depth understanding of the specifics of monetary merchandise, enterprise technique, advertising, psychology, human habits and digital expertise.

Guarantee your inhouse or outsourced crew has a correct monetary CX design course of in place that requires experience in monetary enterprise evaluation, monetary CX analysis, monetary CX structure, and monetary CX technique.

5. Funds Deficit

There are nonetheless corporations that understand monetary providers CX/UX design solely as a visible design that is a part of advertising or product departments receiving a small fraction of the funds. The reality is, within the digital world, enterprise success depends on digital

channels, and accordingly, digital buyer expertise and this ought to be the highest precedence.

To create a powerful digital benefit, prioritize monetary buyer expertise design in technique, processes, crew and budgeting. It doesn’t suggest you want an enormous funding, however a cultural transformation. Switching from push-sales method to customer-centricity

can result in disruptive merchandise that delight customers, convey nice demand and loyalty.

6. No Strategic Context

Generally the monetary business tends to understand UX designers as artists that draw some buttons. Whereas in actuality, monetary UX / CX design consultants carry out equally to enterprise consultants who analysis all associated contexts to creating the digital product

and establish bottlenecks to seek out acceptable options.

For a lot of companies, it is nonetheless not straightforward to outline buyer context. There are corporations that are not conscious of why the purchasers use their service or decline it, additionally they do not test product opinions on the App Retailer or social media, although these are the

primary channels of consumption these days.

7. Bewitched by Innovation

Within the rush for excellent aggressive benefit, many banks search modern applied sciences that may fascinate customers. On the similar time, their current digital options are removed from good and are stuffed with friction that confuse customers. A fancy new innovation

is tough to combine whereas there are a number of points with delivering good buyer expertise in monetary providers by means of the prevailing merchandise.

There isn’t any must reinvent the wheel. Within the majority of instances, patterns and options which can be already acquainted to customers may very well be used.

The very best digital innovation is one which takes the worth for the client to the following stage. This requires completely clear and nice to make use of service, which turns into a robust aggressive benefit of the enterprise.

8. Ignoring the Irrational

Buyer-centricity can’t be achieved correctly by means of numbers alone. Knowledge-driven design is an especially highly effective method. The chance to statistically justify and measure the design end result could be very promising, particularly for the BFSI (Banking, monetary

providers and insurance coverage) business. The darkish facet of it may very well be the accountability shift from product homeowners and designers to knowledge.

Sadly, knowledge cannot bear in mind person habits and emotional context that’s variable and adjustments with time. As Henry Ford acknowledged, “If I had requested individuals what they needed, they might have mentioned quicker horses.” Clients habits, on the whole, is

affected by human irrationality, that is why knowledge gives solely interpretations, not the actual solutions.

9. Over-That includes

There is a frequent false impression amongst numerous FIs – the extra features we offer, the higher the satisfaction of various sorts of our customers will probably be. Truly, it is fairly the other. When a buyer is confronted with loads of choices it confuses him

and results in resolution paralysis. In the long run, the client quits with out taking any motion in any respect and there is a query if he will probably be keen to return again.

Discover out the precise buyer wants and tailor the providers upon them, offering a easy, clear, and intuitive buyer expertise in monetary providers.

10. Underestimating Feelings

For years, banking has been perceived as a really severe establishment that some are even afraid of. The world is altering and so is the finance business. Folks search an emotional connection and a customized angle from their providers, and banking isn’t any

exception.

People are emotional beings by nature. As Don Norman, the apologist for emotional design demonstrates in his works – aesthetics convey worldwide fame even to the best issues like a teapot. It is as a result of it causes the customers constructive feelings and gives

a model new, extra significant expertise.

Take a look at my weblog about monetary and banking UX design >>

The contents inside the article have been equipped through Newswire for Finencial.com, go to

{kind=link}