solely .48 shipped!")

")

By Komson Silapachai

Content material continues under commercial

Final week proved to be a catalyst-filled week with a flurry of information – a powerful jobs report, the FOMC dismissing a March fee reduce, a resumption of regional banking stress, and lower-than-expected Treasury issuance.

Bond yields endured a wild experience, falling precipitously in response to banking considerations, solely to skyrocket in response to the sturdy job numbers. The yield on 10-year treasuries ended up down 11 foundation factors (bps), after falling by 32 bps on the week by Thursday. Two-year Treasuries have been amazingly near unchanged for the week, increased by solely 2 foundation factors, regardless of a pointy transfer decrease and subsequent rise after the roles report.

Credit score spreads continued to point out resiliency. Funding grade (IG) company spreads widened barely through the week, from 92 bps to 96 bps. Regardless of the curler coaster, fastened earnings was constructive on the week with the Combination Bond Index returning +0.65%.

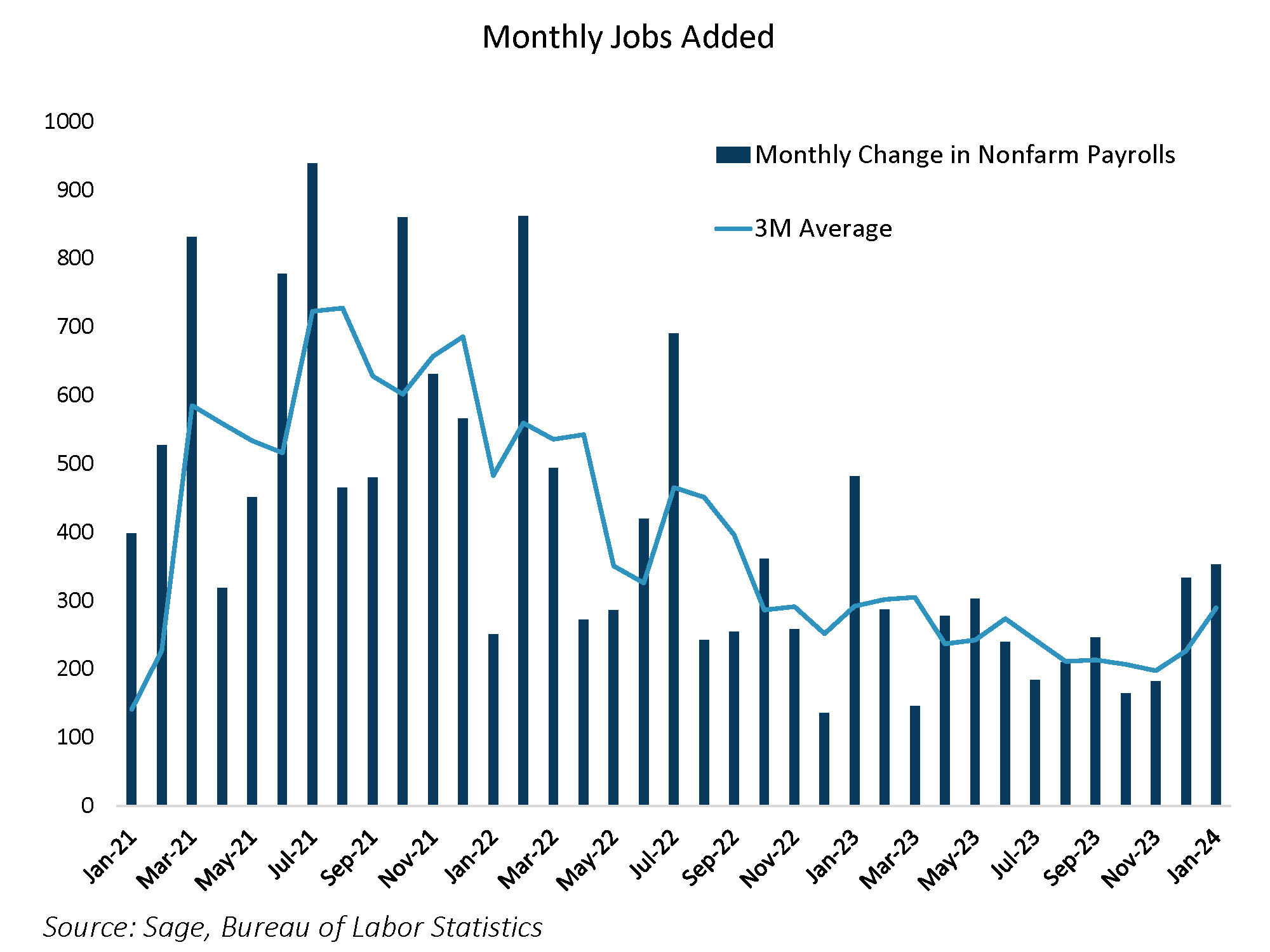

The Jobs Numbers Have been Spectacular

January job numbers quashed any doubt of a powerful financial atmosphere underpinned by a strong labor market. Nonfarm payrolls rose by 353k in January, nicely above the best financial forecasts, whereas the tempo of job development for December was revised up by 117k to 333k. The unemployment fee was anticipated to rise to three.8% however held regular at 3.7%. The good points in jobs have been broad-based, with the Employment Diffusion Index (EDI) rising to its highest level in 12 months at 65.6%, which means extra industries have been including than chopping jobs (impartial is 50%).

If there have been any negatives to the report, common hourly earnings elevated by 0.55% month over month, however the rise in wages shouldn’t be sufficient to throw the Fed astray. The development of underlying job development as illustrated by the 3-month common nonfarm payrolls prints reversed a current decelerating development. It was a powerful print throughout the board.

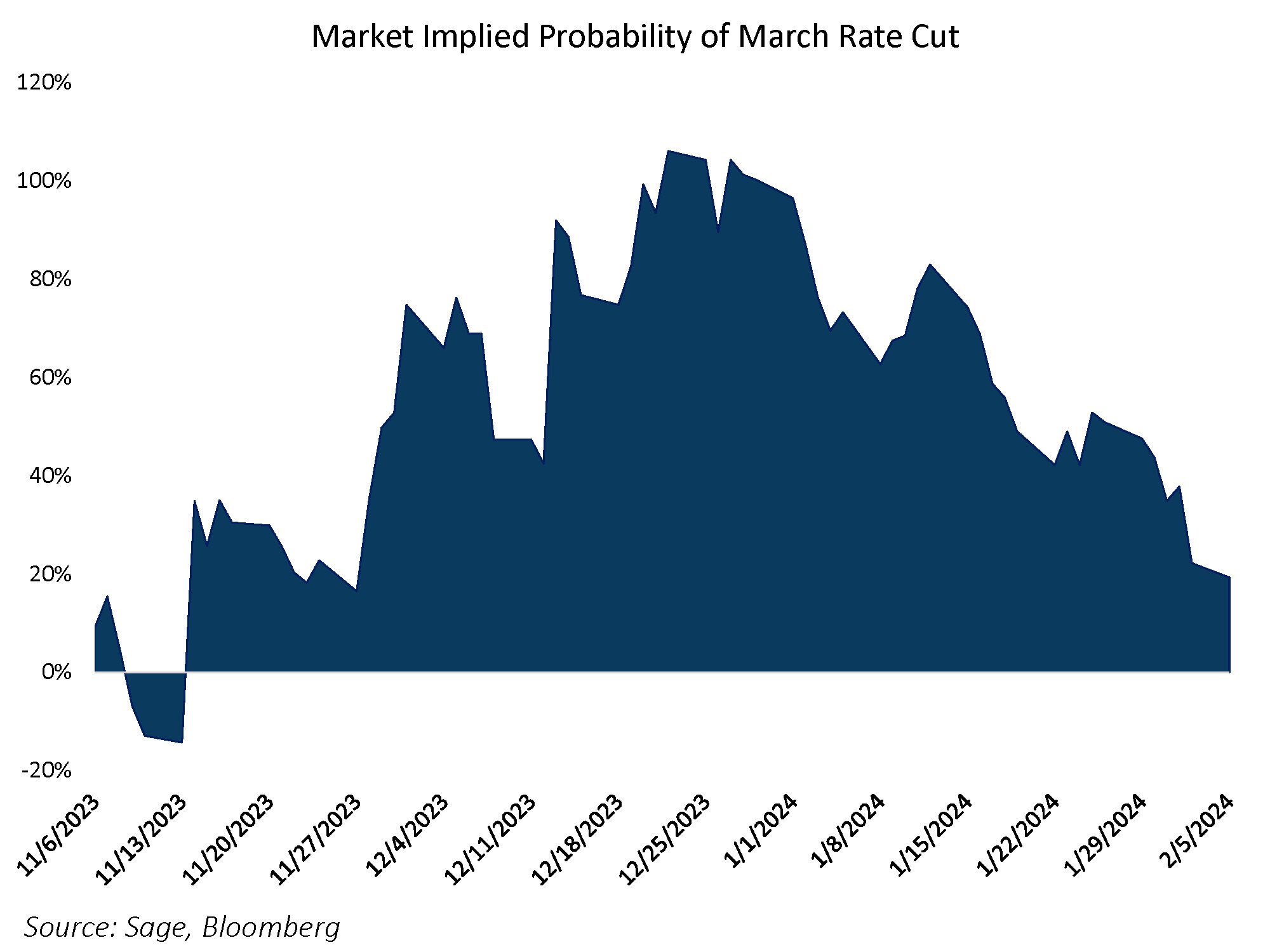

Powell Guidelines Out a March Lower

The primary FOMC assembly of the 12 months didn’t lead to any coverage shifts, and the strong labor knowledge took a March coverage fee reduce off the desk. Within the press convention, Fed Chair Jerome Powell mentioned it was unlikely “that the Committee will attain a degree of confidence by the point of the March assembly,” and {that a} March rate of interest reduce was “not the almost definitely case.”

In November, the Fed’s framework essentially shifted (as indicated by the Waller speech) from preventing inflation to preserving development. Knowledge issues within the timing of when, not if, the Fed flips to a rate-cutting cycle. Powell acknowledged that the committee doesn’t “have a look at [stronger growth]as an issue,” so long as inflation continues to say no. The distribution of outcomes for yields nonetheless skews decrease because the Fed continues to be inclined to chop rates of interest sooner or later within the first half of the 12 months to decrease the extent of actual rates of interest relative to financial exercise.

Nonetheless, rate of interest cuts are actually priced to begin in Could. The likelihood of an rate of interest reduce in March as implied by rate of interest derivatives was 100% to start out the 12 months and now stands at 18% (as of the open of Asian markets on Sunday night).

Decrease Treasury Issuance Boosts Sentiment

Treasury issuance has been a significant danger issue for markets since mid-2023, so markets have been hyper centered on the Fed’s Quarterly Refunding Announcement, which lays out the plan for bond issuance over the approaching quarter. Within the assertion, the Treasury introduced its marketable borrowing for the upcoming quarter of $760 billion, which is decrease than the $815 billion anticipated. The smaller borrowing quantity was on account of a “projection of upper internet fiscal flows and the next starting of quarter money steadiness.” On condition that the quarter consists of the April tax deadline, the Treasury presumably expects tax receipts to be strong this 12 months. The Treasury additionally acknowledged that it does “not anticipate needing to make any additional will increase in nominal coupon or FRN public sale sizes, past these being introduced.” Moreover, T-bill issuance is predicted to lower considerably over the approaching quarter, assuaging considerations round a liquidity drain.

Decrease issuance means much less funds should purchase the newly issued bonds and can be utilized as an alternative for financial exercise and/or investing. General, decrease issuance is a internet constructive for the financial system and markets. Treasury Secretary Janet Yellen continues to be discovering methods to be a dove even in conducting fiscal coverage.

Regional Financial institution Considerations Return

If there was a black swan in a full week of information, it was the resumption of regional banking stress. New York Group Bancorp, which acquired a part of Signature Financial institution final 12 months, stunned markets by saying a loss for the quarter, slashing its dividend, whereas additionally stockpiling an enormous quantity of reserves to cope with future potential mortgage losses. The next night time Aozora, a Japanese financial institution with heavy workplace publicity, additionally stunned markets by saying a internet loss and offering a grim outlook for the US workplace market. The stress unfold throughout the regional banking class, with the KBW Nasdaq Regional Banking Index falling 7.2% on the week.

We’ll proceed to observe the banking story unfold, however it doesn’t look like a market-wide situation proper now. And whereas traders have been caught off guard by the energy in job development during the last two months, our view stays unchanged – the Fed will reduce charges this 12 months; it’s a query of when. This supplies a cap to charges and helps our continued favorable outlook for fastened earnings over the following 12 months.

For extra information, data, and evaluation, go to the ETF Strategist Channel.

Disclosures: That is for informational functions solely and isn’t meant as funding recommendation or a proposal or solicitation with respect to the acquisition or sale of any safety, technique or funding product. Though the statements of truth, data, charts, evaluation and knowledge on this report have been obtained from, and are based mostly upon, sources Sage believes to be dependable, we don’t assure their accuracy, and the underlying data, knowledge, figures and publicly out there data has not been verified or audited for accuracy or completeness by Sage. Moreover, we don’t signify that the knowledge, knowledge, evaluation and charts are correct or full, and as such shouldn’t be relied upon as such. All outcomes included on this report represent Sage’s opinions as of the date of this report and are topic to alter with out discover on account of varied components, resembling market situations. Buyers ought to make their very own selections on funding methods based mostly on their particular funding aims and monetary circumstances. All investments comprise danger and will lose worth. Previous efficiency shouldn’t be a assure of future outcomes.

Sage Advisory Providers, Ltd. Co. is a registered funding adviser that gives funding administration companies for a wide range of establishments and excessive internet value people. For added data on Sage and its funding administration companies, please view our web site at sageadvisory.com, or consult with our Type ADV, which is accessible upon request by calling 512.327.5530.

The contents inside the article have been equipped by way of Newswire for Finencial.com, go to

{kind=link}