solely .48 shipped!")

")

PayTM is the primary digital fee product I’ve used at scale in India.

When RBI enforced the 2 issue authentication mandate for on-line funds, invoice funds grew to become a serious PITA. By requiring customers to fill bank card quantity, expiration date, and half a dozen fields, Reg 2FA precipitated great friction. After they obtained

the OTP, entered it and hit the submit button, many customers – me included – incessantly skilled failed funds. Extra at

Why Two Issue Authentication Is A “Conversion Killer” & “Blood Stress Booster” and Going From Card To COD. (hyperlink to put up on my firm web site eliminated to adjust to Finextra Neighborhood Guidelines however these posts ought to seem

on prime of Google Search outcomes when searched by their title + “GTM360”)

Pissed off by this expertise, I craved for an digital pockets that I may prime up with a lumpsum quantity from my bank card as soon as a month and use the steadiness to pay all my month-to-month payments with out being topic to friction and risking failure of every fee.

PayTM fulfilled that want. Whereas PayTM prolonged help for UPI and UPIlite a lot later, I am speaking concerning the time when it had just one mode, particularly, pockets, and put via on-line funds with out OTP and even

password. In different phrases, PayTM blatantly subvented two issue authentication. RBI seemed the opposite approach.

Though Indians are alleged to be very security-conscious, they lapped up PayTM by the hundreds of thousands regardless of its lax safety. On the peak, PayTM had 100 million pockets customers, which was greater than the shopper base of any financial institution in India. By way of the years, I’ve

written many posts on this weblog about PayTM’s revolutionary method in the direction of pockets topup, PUSH notifs, OTP SMS, autofill OTP, soundbox, feet-on-street gross sales and its rise to turn out to be a

blockbuster hit.

By proving that the sky did not fall on account of its nuanced method in the direction of safety, I am guessing that PayTM formed the design of UPI. Not like the earlier on-line funds that mirrored the regulator’s historic bias in the direction of safety, UPI leans in the direction of comfort

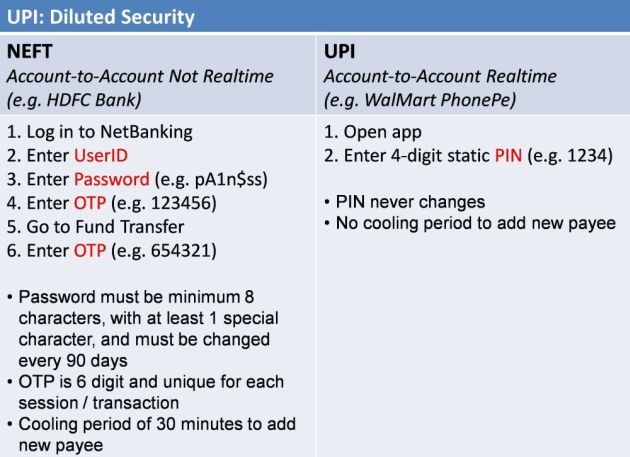

and superior consumer expertise. As described within the following exhibit, UPI has approach much less safety than NEFT, IMPS and different strategies of funds that contact a checking account.

Quick ahead to 31 January 2024.

RBI ordered PayTM to cease operations by finish of February.

The regulator took this unprecedented step after its complete techniques audit uncovered persistent non-compliances and continued materials supervisory considerations in

PayTM Funds Financial institution (PPB).

The purpose to notice is that RBI’s enforcement motion is focused solely on the funds financial institution affiliate of the publicly traded fintech known as One97 Communications Restricted aka PayTM.

PayTM presents a variety of economic providers services and products comparable to funds, FASTag (pay as you go freeway toll product), NCMC (pay as you go public transport ticketing), client credit score, service provider credit score, fee gateway, and so forth. (PayTM’s utility for

Cost Aggregator aka Service provider Aggregator was not authorized by RBI). A few of these merchandise / providers are rooted in PPB, some are impartial of PPB and a few straddle each corporations. Whereas PPB has “financial institution” in its title, it can not do any lending since it is a funds

financial institution, which is a restricted type of banking constitution that permits deposit-taking however not lending.

———-

@s_ketharaman: Financial institution that may’t lend could make income – and revenue – through charges on its funds merchandise, rake on bancassurance, and distinction

in curiosity between what it will get from authorities bonds and what it pays to depositors.

———-

Quickly after RBI’s announcement, I speculated the next non-compliances and oversight considerations with PayTM, within the growing order of severity (not authorized recommendation however they go from a mere rap on the knuckles via to fantastic and jail time):

- Did not give sufficient bhaav (respect in Hindi) to RBI / exterior auditors

- Skimmed MDR from financial institution to mother or father firm

- Used financial institution’s steadiness sheet for mother or father firm’s lending enterprise

- KYC violations

- Cash laundering.

In accordance with the largely speculative media reporting within the following 2-3 days, all 5 have emerged as extremely probably elements behind the regulator’s harsh motion. The media has clubbed the second and third factors beneath the catch-all expression “breach of

arms size relationship between associated events”. Extra in

The Morning Transient podcast.

———-

In accordance with

McKinsey, fintech gamers are “start-ups and progress firms that rely totally on expertise to conduct elementary features offered by monetary providers, thereby affecting how customers retailer, save, borrow, make investments, transfer, pay, and defend cash”.

Once they begin off, fintechs haven’t got a banking license, and associate with sponsor banks to supply checking accounts, financial savings accounts, loans, and different banking merchandise. Over time, some fintechs apply for and get a banking constitution and turn out to be a financial institution themselves.

PayTM is the one fintech I do know that is not a financial institution, which not solely works with sponsor banks but additionally has an inhouse financial institution (One97 has 49% stake in PayTM Funds Financial institution, the opposite 51% of which is held by its founder Vijay Shekhar Sharma in his private capability.)

In my time, I’ve come throughout many (completely kosher) deal buildings, monetary engineering and company labyrinths however I have not seen something like what PayTM has accomplished right here.

I can think about the insane quantity of complexity brought on by PayTM’s product, service and company construction in how safety, knowledge privateness, and wall cross legal guidelines apply to it. A few days after RBI cracked down on it, PayTM advised the Financial Instances that its

financial institution “couldn’t fulfill the banking regulator concerning compliance and expertise”.

I am not stunned. Whereas I am being a bit beneficiant to PayTM right here, most regulators have giant egos and tunnel imaginative and prescient and may’t tolerate artistic interpretations of the foundations they’ve written. Exhibit Z: Coinbase v. SEC in USA.

RBI seemed the opposite approach when PayTM subvented 2FA previously however it has clamped down on the fintech large now.

———-

Startup Bros and VCs have lamely copied Adani Group’s response to

Hindenburg Analysis’s hit job round this time final yr, and have known as RBI’s motion an assault on fintech shoppers and the general startup ecosystem. That is self-serving BS.

https://twitter.com/s_ketharaman/standing/1753756854188908711

Some trade observers say the regulator’s motion is disproportionate e.g Nikhil Pahwa in his op-ed titled

RBI shouldn’t be match to manage digital funds within the Financial Instances. For my part, the creator is conflating

coverage with enforcement motion. Let me clarify.

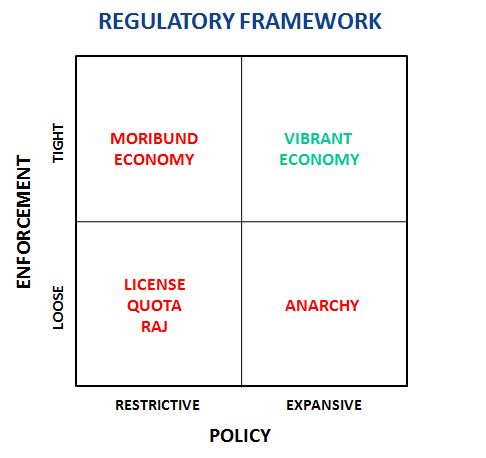

The regulator’s newest transfer is a case of enforcement motion in opposition to a particular firm, particularly, PayTM Funds Financial institution. Not like the creator, I imagine that tight enforcement is critical with a view to be sure that the financial system does not go rogue. In accordance with my supreme

regulatory framework displayed within the exhibit on the fitting, expansive coverage mixed with tight enforcement is one of the best recipe for a vibrant financial system in a capitalism.

RBI’s coverage stance is akin to “Freeway may cause accidents, we should always ban freeway”. Which is clearly lame. Whereas its stance on enforcement is akin to “We’ll come down on one flawed aspect driver in such a approach that no one else will drive on the flawed

aspect of the freeway”. Which is ok.

Whereas the previous stance thwarts innovation and progress, I can consider many examples the place the latter has proved extremely efficient.

- Ticketless journey in Germany. At any time when a prepare ticket examiner caught a ticketless traveler in an S-Bahn in Frankfurt, she’d deboard the offender on the subsequent station. 5 extra TTEs within the prepare would be part of her on the platform. All six of

them would encompass the ticketless traveler and march him up and down the platform in order that the entire prepare would see the poor sod’s stroll of disgrace. (For the uninitiated, S-Bahn or Schnell Bahn i.e. Quick Rail is among the a number of modes of speedy transit in

German cities, the others being U-Bahn, Str-Bahn and Omnibus). - Powell Doctrine in USA. Though Shock and Awe and Strike with Overwhelming Pressure are customary American warfare techniques, the present crackdown by OCC on Blue Ridge Financial institution and lots of BaaS suppliers is a nod to this method within the American banking

trade. - Masks mandate in India. Through the pandemic, the second anyone out of a posse of 5 visitors cops noticed a maskless motorist in Pune, all 5 of them piled on to her or him. Even when a number of maskless motorists slipped away within the ensuing

circus, everybody received a loud and clear message that legislation enforcement was critical about imposing the foundations on sporting masks.

Whereas it’d come throughout as a tad unfair to the solitary offender, tight enforcement works so long as it isn’t barbaric. As governments turn out to be lean and slash headcount in authorities businesses, disproportionate enforcement could be the one pragmatic mannequin

of guaranteeing order going ahead.

———-

Pathbreaking enterprise mannequin innovators like AirBnB,

Reliance and

Uber have been shrouded beneath the regulatory cloud for a lot of their company existence however finally they’ve persuaded the powers-that-be that their enterprise fashions are “not unlawful”.

Time will inform whether or not PayTM will have the ability to do the identical.

https://twitter.com/s_ketharaman/standing/1313456555522752513

The contents throughout the article have been equipped through Newswire for Finencial.com, go to

{kind=link}