solely .48 shipped!")

")

Traditionally, buyers have bought bonds for his or her regular coupon funds. This relationship was thrown on its head because the Fed minimize charges within the wake of the Nice Disaster. Value appreciation as charges fell grew to become the secret. That’s, till final yr when the broader bond market fell.

Nonetheless, based on funding supervisor Thornburg, that will not be such a nasty factor for the municipal bond market.

Due to a wide range of elements, worth appreciation within the muni bond market could also be onerous to return by. However with such ample tax-equivalent yields, which may not be a problem for buyers. Earnings will drive the bus and that may nonetheless result in nice returns.

Breaking the Development

With rates of interest hitting highs not seen in a few decade, it’s simple to overlook that only a yr or two in the past, buyers had been scrambling for yield. General, charges have been falling for the reason that Eighties. Then an unprecedented zero-rate curiosity coverage began on the finish of the Nice Recession. The severity of the recession required the Fed to drop rates of interest to zero to jumpstart the financial system. And with gradual progress and low inflation, the central financial institution stored them there for roughly a decade.

Bonds have an inverse relationship with charges. So, when charges drop, buyers flock to older, higher-yielding bonds for earnings. This creates worth appreciation.

For the municipal bond market, that worth appreciation was fairly good. The Bloomberg Municipal Bond Index managed to have a streak of eight consecutive years of constructive complete returns – aka yield plus worth appreciation. Even when the Fed raised charges by 0.25% in 2015, munis nonetheless managed to provide a slight achieve. You need to return to the so-called ‘Taper Tantrum’ of 2013 for the sector to point out a loss.

Nonetheless, the nice occasions ended final yr. Because the Fed raised charges to fight surging inflation, bonds of all types had their worst years in a very long time. That included munis. In 2022, the Bloomberg Municipal Bond Index posted its worst complete return in additional than 30 years: a detrimental 8.8%.

A Sturdy 2023 & Past

However that poor efficiency in 2022 could result in a powerful constructive one for muni bonds going ahead. In keeping with evaluation from funding supervisor Thornburg, muni bonds’ juicy after-tax yields will assist these bonds carry out nicely this yr and past.

In keeping with the funding supervisor, many buyers who purchased bonds over the previous couple of years did so in a bizarre interval as falling charges drove up costs. That’s not regular for the sleepy muni market. Taking a look at knowledge for the final 30 years, simply over 90% of the full return of the Bloomberg Municipal Bond Index comes from earnings and fewer than 10% has been pushed by worth good points.

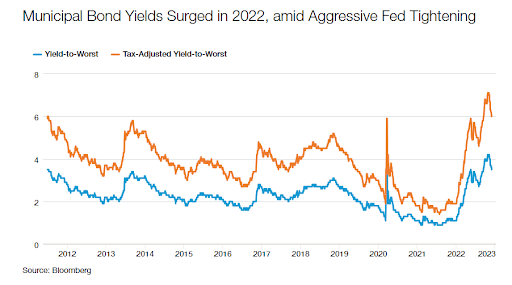

And proper now, yields are at a few of their largest factors in 12 years. Simply check out this chart from Thornburg. Proper now, buyers within the highest tax brackets can rating tax-equivalent yields of 6%, whereas these within the median 24% can nonetheless earn roughly 4% on their cash. This doesn’t even embrace the impact of state and native taxes on that yield.

Supply: Thornburg Investments

In keeping with Thornburg, that units up an excellent place for munis to ship constructive and powerful returns going ahead. That prime beginning yield supplies sufficient of a ‘cushion’ that munis shouldn’t unload in worth by an excessive amount of if there’s a downturn. Higher nonetheless is that top yield is tax-free for many buyers. Value appreciation just isn’t.

Furthermore, Thornburg suggests the character of muni patrons will assist as nicely. Traditionally, munis have been a spot for rich people to purchase and maintain. Today, municipal bonds are actually discovering their methods into a wide range of professionally managed and institutional investor portfolios. For instance, insurance coverage and pension funds are actually a number of the greatest patrons of muni bonds. This has created one other purchaser worth ground for the asset class. Final yr’s patrons had been largely the so-called yield vacationers. Now a steadier purchaser base is right here, able to sop up provides amid these excessive yields.

On the identical time, municipal credit score high quality shouldn’t be ignored. State’s wet day funds are at their fattest quantities on report, whereas the huge bulk of the sector trades at excessive credit score scores. This places it on par with U.S. authorities debt. When factoring within the tax benefits of the sector, it turns into much more advantageous.

So, whereas munis could not see large worth good points over the few years, returns will likely be sturdy, pushed by their hefty coupon funds.

Shopping for Some Muni Earnings

With munis providing sturdy yields and the potential for that yield to drive returns, buyers could need to comply with Thornburg’s recommendation and begin aggressively including munis to their portfolios. Shopping for them individually remains to be a tough area to play on, with many munis buying and selling on the OTC exchanges and new points being oversubscribed. However given the dimensions of the muni market, there are quite a few methods to get your fingers on the bonds.

Munis are one of many few asset courses that profit from energetic administration, with the majority of managers beating their benchmarks over the lengthy haul. Prime funds just like the PIMCO Intermediate Municipal Bond Energetic ETF or Thornburg’s personal Intermediate Municipal Fund make tremendous portfolio additions to play the earnings potential in municipal bonds.

Nonetheless, the query is whether or not or not energetic administration will make a distinction within the present setting. In spite of everything, yield and the earnings that these bonds throw off will drive returns going ahead. To that finish, buyers could solely must index to get juicy returns.

At $32 billion in belongings, the iShares Nationwide Muni Bond ETF is the biggest ETF within the sector and provides a low-cost method so as to add muni bonds to a portfolio. To not be outdone, the Vanguard Tax-Exempt Bond Index Fund and SPDR Nuveen Bloomberg Municipal Bond ETF will also be used for reasonable beta publicity to the asset class. With the ETFs, supervisor talent is placed on maintain they usually can coupon clip to get the returns. For instance, the iShares’ fund is yielding a tax-equivalent 6.4% for an investor within the prime tax bracket.

Municipal Bond Mutual Funds & ETFs

These funds had been chosen based mostly on their YTD complete return, which vary from -3.2% to 2.4%. They’ve bills between 0.05% to 0.91% and have belongings underneath administration between $40 million to $33 billion. Their yields are between 1.4% to three.6%, which works out to be a tax-equivalent vary of 1.82% to 4.37% for somebody within the 24% median tax bracket.

| Ticker | Identify | AUM | YTD Complete Ret (%) | Yield (%) | Exp Ratio | Safety Kind | Actively Managed? |

|---|---|---|---|---|---|---|---|

| MEAR | BlackRock Brief Maturity Municipal Bond ETF | $509M | 2.4% | 3.6% | 0.25% | ETF | Sure |

| PVI | Invesco VRDO Tax-Free ETF | $41M | 2.1% | 3.6% | 0.25% | ETF | No |

| FGNSX | Strategic Advisers Tax-Delicate Brief Length Fund | $4.19B | 1.8% | 3.1% | 0.37% | MF | Sure |

| PSMEX | Putnam Brief-Time period Municipal Earnings Fund | $52.1M | 1% | 2.9% | 0.91% | MF | Sure |

| THIMX | Thornburg Intermediate Municipal Fund | $899M | 0.1% | 3.3% | 0.91% | MF | Sure |

| SUB | iShares Brief-Time period Nationwide Muni Bond ETF | $9.59B | -0.3% | 2% | 0.07% | ETF | No |

| MUNI | PIMCO Intermediate Municipal Bond Energetic ETF | $1B | -0.4% | 3.5% | 0.35% | ETF | Sure |

| MUB | iShares Nationwide Muni Bond ETF | $32.8B | -1.8% | 2.9% | 0.07% | ETF | No |

| SHM | SPDR Nuveen Bloomberg Brief Time period Mun Bond ETF | $4.06B | -1.0% | 1.4% | 0.20% | ETF | No |

| PZA | Invesco Nationwide AMT-Free Municipal Bond ETF | $2.33B | -1.8% | 2.9% | 0.28% | ETF | No |

| VTEB | Vanguard Tax-Exempt Bond Index Fund | $30.6B | -1.8% | 3.1% | 0.05% | ETF | No |

| ITM | VanEck Intermediate Muni ETF | $1.81B | -2.2% | 2.4% | 0.24% | ETF | No |

| TFI | SPDR Nuveen Bloomberg Municipal Bond ETF | $3.8B | -3.2% | 2.7% | 0.23% | ETF | No |

Maybe one of the best play may very well be to pair a passive ETF for broad muni publicity and an energetic fund. Finally, the mix might show to be one of the best fruitful final result for buyers.

Both method, municipal bond yields are at a few of their highest factors in years. That means the bonds will present sturdy returns going ahead with that yield offering many of the good points. That’s not essentially too shabby.

The Backside Line

After final yr’s rout, municipal bonds are providing tax-equivalent yields north of 6%. In keeping with funding supervisor Thornburg, that’s an enormous win for buyers, with that yield driving a lot of the sector’s potential return. Below that guise, muni bonds are a giant purchase. Pairing a passive ETF with an energetic fund might present one of the best mixture of returns for the sector.

The contents throughout the article have been provided through Newswire for Finencial.com, go to

{kind=link}