solely .48 shipped!")

")

Confluence Funding Administration presents numerous asset allocation merchandise that are managed utilizing “prime down,” or macro, evaluation. We publish asset allocation ideas on a bi-weekly foundation, updating the report each different Monday, together with an accompanying podcast.

Content material continues under commercial

As of late, as a result of traders have so many alternative belongings to purchase in so many alternative monetary markets, it may be straightforward to overlook an vital development or change in development. Certainly, that appears to be the case with crude oil, the place the lengthy stagnation in U.S. output after the COVID-19 pandemic has instantly became a brand new surge. Actually, U.S. oil manufacturing has not too long ago reached a brand new file excessive. On this report, we discover what allowed home output to start out increasing once more, what it means for the worldwide financial system, and the potential implications for traders.

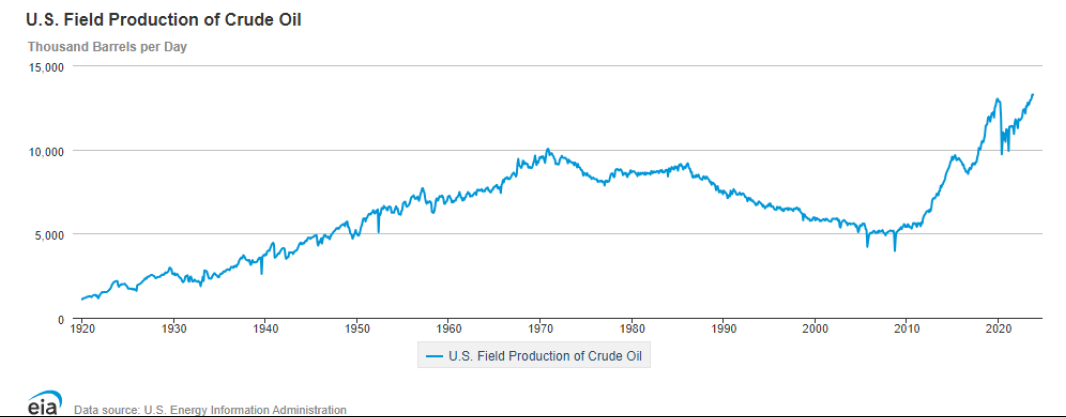

As proven within the chart under, U.S. area manufacturing has fluctuated fairly a bit over the past century. From 1920 to 1970, output grew roughly 4.2% per 12 months, reaching 9.6 million barrels per day (bpd). Nevertheless, output then fell and plateaued, regardless of the incentives to provide through the interval’s excessive costs. Starting in about 1985, manufacturing started what gave the impression to be an inexorable decline within the face of public coverage and the boundaries of the accessible know-how. To many individuals’s shock, output instantly reversed and began rising quickly once more through the Nice Monetary Disaster of 2008-2009, pushed by new applied sciences equivalent to hydraulic fracturingand horizontal drilling that opened up beforehand untappable shale formations. U.S. manufacturing jumped at an annual price of 8.7% from 2009 to 2019, reaching nearly 13.0 million bpd.

Clearly, the pandemic was a shock to the worldwide financial system. With the collapse in demand, oil costs truly turned damaging for a short while in early 2020. Extra importantly, U.S. output fell sharply and appeared to stagnate. A lot of the stagnation mirrored lowered funding in new exploration and improvement as traders demanded higher capital self-discipline and a stronger deal with profitability after the various bankruptcies of shale drillers through the interval of 2009-2019. Stronger environmental rules, which aimed to shift the financial system away from fossil fuels, additionally discouraged drilling. Many traders started to query whether or not the business may ever develop once more.

In mid-2023, U.S. oil output started to speed up in earnest, probably reflecting the inducement of excessive vitality costs on the time and an surprising second wind from know-how enhancements. Press experiences say fracking and different shale applied sciences in addition to working approaches have merely improved greater than anticipated. In any case, U.S. oil output has now reached 13.3 million bpd.

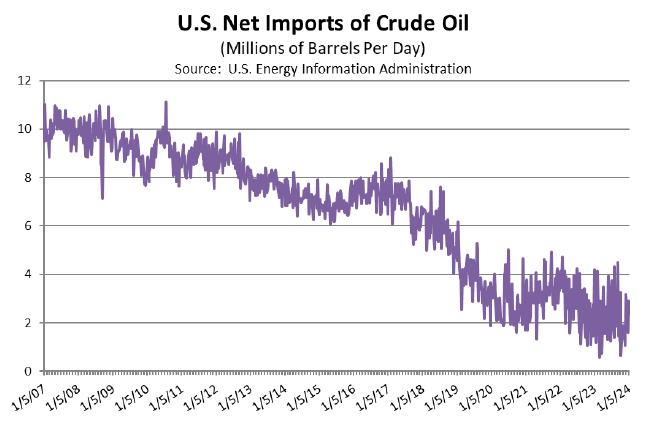

For the worldwide financial system, booming U.S. oil output doesn’t simply imply that the nation has change into the world’s largest producer (which it has). As proven within the chart under, it additionally signifies that the U.S. has been capable of considerably cut back its imports of overseas oil.

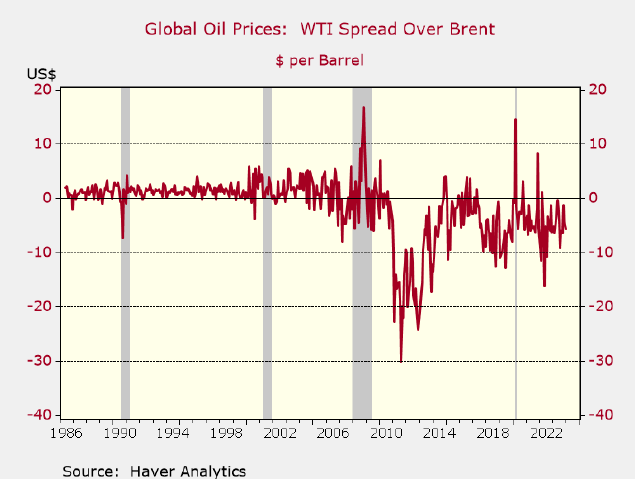

Surging U.S. oil manufacturing has altered international pricing dynamics. For instance, earlier than the shale increase, U.S. home oil costs (represented by the West Texas Intermediate) have been usually barely greater than overseas costs (represented by Brent Crude). For the final decade, nevertheless, the wealthy provide of home oil has held down U.S. costs. Decreased U.S. import demand and new legal guidelines permitting U.S. oil exports have additionally improved provides for different nations. As proven within the following chart, Brent Crude now tends to commerce a number of {dollars} greater than WTI. Nonetheless, the U.S. adjustments haven’t been sufficient to completely offset the truth that Saudi Arabia and its companions in OPEC and OPEC+ are withholding provides with a purpose to increase costs.

Going ahead, the surprising rebound of U.S. oil output and exports signifies that American manufacturing may assist maintain a lid on international costs for an prolonged interval, even because the OPEC+ nations proceed to withhold barrels. What may change the outlook? One key threat that we’re centered on is the opportunity of a geopolitical disaster that disrupts provides from a serious overseas producer or exporter. If such a disaster happens outdoors the Center East, the supply of extra output capability in Saudi Arabia and the remainder of OPEC+ may probably fill within the hole. If the disaster disrupts Center Japanese provides, nevertheless, the end result would probably be a spike in international costs regardless of the renewed U.S. output increase and extra manufacturing capability within the area.

For extra information, data, and evaluation, go to the ETF Strategist Channel.

Previous efficiency isn’t any assure of future outcomes. Info supplied on this report is for instructional and illustrative functions solely and shouldn’t be construed as individualized funding recommendation or a suggestion. The funding or technique mentioned is probably not appropriate for all traders. Buyers should make their very own choices based mostly on their particular funding targets and monetary circumstances. Opinions expressed are present as of the date proven and are topic to alter.

This report was ready by Confluence Funding Administration LLC and displays the present opinion of the authors. It’s based mostly upon sources and knowledge believed to be correct and dependable. Opinions and forward-looking statements expressed are topic to alter. This isn’t a solicitation or a proposal to purchase or promote any safety.

The contents throughout the article have been equipped through Newswire for Finencial.com, go to

{kind=link}